2025: The Year Distribution Became the Dealbreaker

Why low-voltage networks are where the energy transition is won or lost—and what it means for infrastructure investors

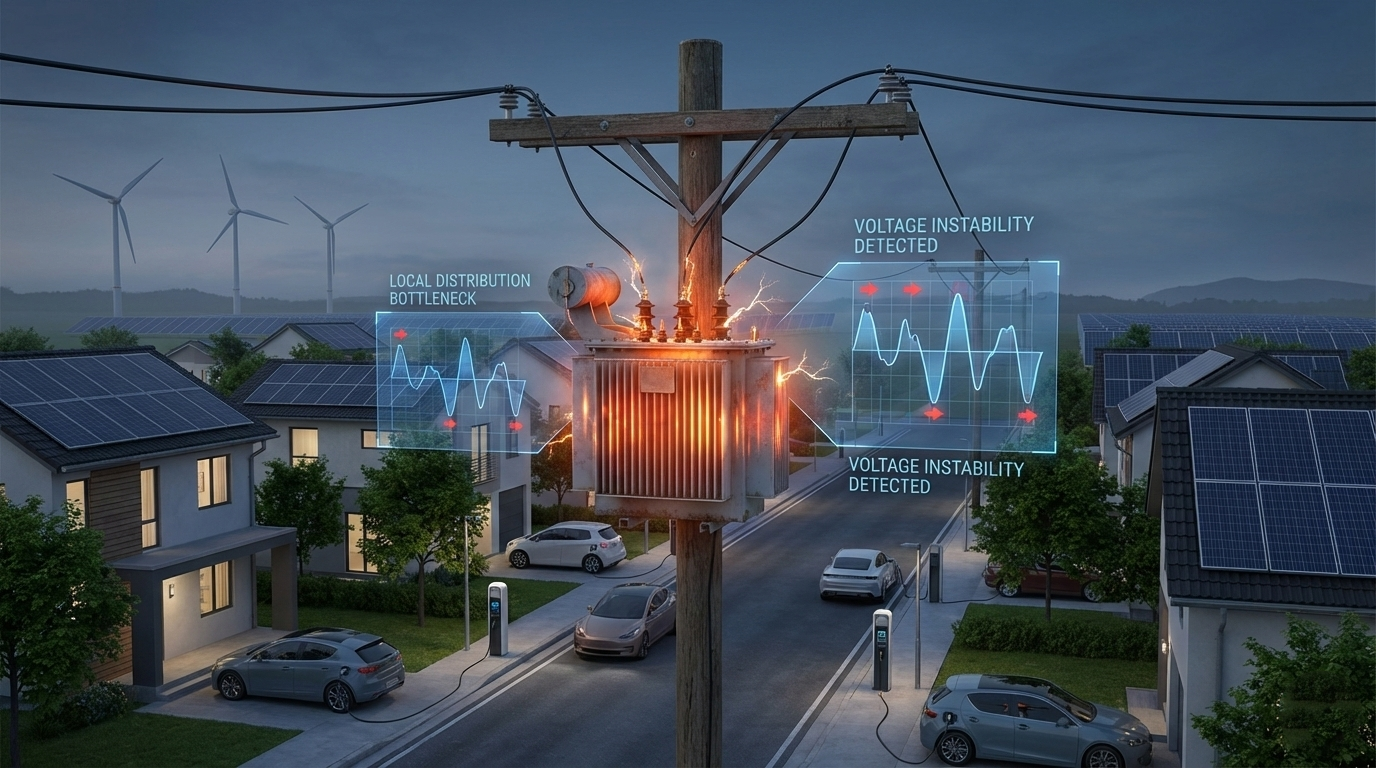

1. The Grid Paradox: We Can Build Everything Except the Last Mile

A 50 MW data centre inQueensland has been waiting 18 months for a grid connection. The site has land,capital, customers, everything except the final 400 meters of low-voltage distribution capacity to turn power on.

In the UK, automotive giant Stellantis was told its warehouse solar installation won't connect until 2035,an 11-year wait for a rooftop array that could be installed inweeks. The company needs that power to meet its 2030 carbon reduction targets,but the grid queue says no.

These aren't isolated incidents.They're symptoms of the defining infrastructure constraint of our time.

In 2025, the global energytransition hit its first major bottleneck. We can build renewables, EVs, heatpumps, and AI data centres at record pace. Still, we cannot connect and operatethem reliably without fundamentally rethinking how electricity moves throughthe last mile of the grid.

The chokepoint isn't at thepower plant or the transmission tower. It's at the neighbourhood transformerand the low-voltage (LV) feeders serving homes, businesses, and EV chargers.

While policymakers debatedcarbon targets and investors poured capital into generation assets, theunglamorous but critical question went unanswered: how do you unlock capacity where the grid actually touches demand?

2025 forced that question intothe open. Across the UK, Australia, Europe, and North America, the same storyrepeated: connection queues measured in years, not months. Voltage violations climbing. Transformer failures accelerating. Solar curtailmentc reating fairness crises.

This is why LV matters more thanmost infrastructure investors realise, and why 2025 became the year theconversation finally shifted from "build more copper and iron" to"unlock what's already there, faster."

2. The Convergence: Why 2025 Made LV Infrastructure Unavoidable

Three forces collided in 2025,all converging at the distribution transformer and LV feeder level. Together, they turned theoretical network constraints into an immediate economic andpolitical crisis.

AI and Data Centres: Load Growth Became a Right-Now Problem

The AI boom stopped being a future scenario and became a near-term grid constraint. The IEA projects globaldata centre electricity consumption will double to ~945 TWh by 2030,growing ~15% annually. Bloomberg NEF's revised forecasts showed the speed andscale catching utilities off guard, not just at transmission, but also at distribution and often at local LV substations feeding clustered demand.

What this means: Capacity, connection speed, and power quality are now directly tied to GDP growth and competitiveness. Grid capex is being reprioritised accordingly, but traditional reinforcement timelines don't match data centre deployment cycles.

The impact hits LV networks first: data centre growth doesn't only stress transmission—it stresses the local substations and feeders that must deliver stable, high-quality power to equipment worth hundreds of millions.

Connection Queues: From Industry Frustration to Economic Crisis

In the UK alone, the grid connection queue reached 722GW in 2024, ten times Britain's current power capacity. NESO's emergency reform cut this to 283GW with offers through 2035. Still, the damage was done: viable projects waited behind "zombie" applications from developers who didn't even own the land.

In 2025, connection delays moved from industry frustration to a headline economic issue:

- 132GW of renewables slated to connect by 2030 in the UK

- 153GW of battery storage projects cut from the queue entirely due to oversupply

- Ofgem's Connections End-to-End Review explicitly framed queue inefficiency as a threat to clean power ambitions and growth

Stellantis wasn't alone:companies across sectors faced 5-, 10-, and even 15-year waits for connections that should have taken months. The bottleneck? Often not transmission capacity, but LV network constraints and a planning system that never anticipated this velocity of demand.

For investors: Any technology or delivery model that shortens time-to-connect or reduces the amount of reinforcement required per connection becomes strategically valuable overnight.

Equipment Supply Chains: Transformers Became the Binding Constraint

While everyone worried about solar panels and battery supply, 2025 revealed that distribution transformers were the real constraint. Wood Mackenzie warned of transformer supply deficits, and NREL reported lead times of ~2 years and significant price increases. Reuters highlighted manufacturing investment driven by soaring demand, but capacity couldn't scale fast enough.

The maths don't work: if you need to replace or upgrade hundreds of transformers annually, but each one takes 18-24 months to procure, you're perpetually behind. This hit residential networks particularly hard, PV and EV growth outpaced forecasts, but the transformers those connections rely on weren't arriving.

"Build more copper and iron" isn't always feasible on the timelines needed. Solutions that do more with what's already installed gained immediate value.

Solar and EV Growth: The LV Layer Shows Stress First

Research across Australia,Europe, and North America confirmed what utilities were seeing in the field: PV, EVs, and heat pumps drive voltage rise, phase imbalance, and harmonic distortion in LV networks.

Australia's Race for 2030 study, analysing a Brisbane suburban network through 2050, found:

- By 2050 under aggressive electrification scenarios, 23.4% of LV buses exceeded voltage limits during midday solar peaks

- Voltage unbalance (VUF) reached 5.7% at the 99th percentile, well above acceptable limits

- 4.4% of PV generation curtailed due to Volt-Watt inverter controls, but unfairly distributed, with customers at feeder ends losing 60% of output while those near transformers lost nothing

EV chargers added their ownstress:

- Single-phase residential charging caused significant phase imbalance and neutral current flow

- Current THD rose to 15-20% during active charging

- Uncontrolled simultaneous charging caused voltage imbalances exceeding 2% regulatory limits

- Transformer overheating from unbalanced loads and harmonic heating

The UK government pushed for better visibility of distributed assets as a prerequisite for operating smarter local networks. Still, visibility alone doesn't solve voltage, imbalance, or thermal stress.

The winners: Technologies that don't just add capacity, but stabilise the network so it can host more DER and electrified load without service degradation.

3. The Industry Response: From "Plan and Build" to"Optimise and Enhance"

2025 wasn't just about problems, it was about the industry pivoting toward solutions that could deploy faster, cheaper, and more flexibly than traditional reinforcement.

Capex Efficiency Over Pure Capex Volume

BloombergNEF flagged global grid investment potentially topping $470bn in 2025. In the UK, Ofgem's network investment announcements kept grids in mainstream press and investor briefings, but capital is increasingly tied to outcomes: deploy faster, defer reinforcement, deliver resilience, protect consumers.

The shift: from "how much can we spend?" to "how much capacity can we unlock per dollar, and how fast?"

Grid-Enhancing Technologies (GETs) Moved Mainstream

ESIG's 2025 report focused on use cases, barriers, and recommendations for scalable GET deployment, a signal the sector shifted from "whether" to "how." Utilities increasingly treated GETs (dynamic line ratings, advanced power flow control, topology optimisation) as scalable infrastructure tools, not pilot curiosities.

But there's a gap: transmission GETs are scaling, but LV remains the neglected layer. This is where DERs, EVs, heat pumps actually connect. Power quality issues (voltage, imbalance, harmonics) emerge here first. Yet LV has the fewest sophisticated tools available.

Flexibility Markets Grew, But Can't Replace "Hard Capacity"

Flexibility is now a core tool for managing peaks and congestion, with UK DSOs positioning it as key to managing demand at lower cost. But flexibility needs stronger, smarter LV beneath it, because you can't dispatch what you can't connect, and you can't rely on flexibility alone where power quality is deteriorating.

Flexibility addresses"when." LV infrastructure addresses "whether", whether the network can physically support the connection at all.

4. Third Equation's Network Exchanger: Built for This Moment

This is where Third Equation enters the picture.

The Network Exchanger (NEx) isa grid-enhancing technology purpose-built for low-voltage distribution,te layer where electrification stress shows up first, and wheretraditional solutions struggle to deploy fast enough.

What NEx Does (Integrated, Not Listed)

NEx addresses the LV capacity constraint at three levels:

1. Capacity Unlocking: Installed at distribution transformers, NEx increases effectivecapacity at the transformer while improving voltage regulation and phase balance, helping networks serve new load without waiting for long lead-time reinforcement or transformer replacement.

2. Power Quality Management: NEx performs three critical functions simultaneously:

- Voltage regulation at the head of LV circuits (independent per-phase control)

- Current balancing across all three phases at the transformer

- Power factor correction to reduce reactive power burden

This combination reduces voltage violations, mitigates unbalanced loading that causes transformer overheating, and improves harmonic performance, all issues exacerbated by PV, EV, and heat pump proliferation.

3. Speed of Deployment: Because NEx works with existing assets rather than requiring major civil works, it installs quickly and repeatedly across fleets of substations, bypassing supply chain delays that plague transformer procurement.

Proof: Race for 2030 Study Results

In independent testing by Monash University (Australia's Race for 2030 program), NEx was evaluated against STATCOMs and On-Load Tap Changers (OLTCs) in six constrained LV areas facing voltage violations and curtailment:

Voltage violations eliminated:

- BAU scenario: 62.9% of buses exceeded voltage limits

- Single STATCOM: 53.4% (modest improvement)

- Multiple STATCOMs: 23.8% (better, but limited by per-circuit placement)

- OLTC: 7.1% (good, but struggled with phase imbalance—uniform tap adjustment worsened under voltage on already-low phases)

- NEx: 0%, complete elimination due to independent per-phase voltage control

Transformer loading reducedsignificantly:

- One example transformer: BAU 150% loading → NEx 122% loading (current balancing + power factor correction + voltage optimization reduced stress)

- Across all six areas, NEx consistently delivered the greatest transformer loading reductions

Curtailment addressed:

- BAU: 108.1 kWh curtailed during spring midday half-hour

- NEx: 5.1 kWh, a 95% reduction while maintaining voltage compliance

Why NEx outperformed:

- OLTCs adjust all three phases uniformly, effective in balanced networks, but can worsen conditions in unbalanced LV networks (common with single-phase PV and EV)

- STATCOMs provide reactive support locally but have limited reach along radial LV circuits

- NEx regulates voltage at the transformer (affecting entire LV area) with independent per-phase control, plus balances currents and corrects power factor, addressing root causes, not just symptoms

Why Now: Strategic Fit with 2025 Market Conditions

NEx aligns with every majortheme from 2025:

- Addresses AI/data centre load growth by unlocking more usable capacity at existing transformers and improving power quality, critical for sensitive IT loads

- Shortens connection timelines by enabling more connections within existing constraints, complementing (not replacing) queue reform

- Works around transformer supply constraints by maximising what's already installed rather than waiting 2 years for new equipment

- Solves the LV power quality crisis that PV and EV growth created, voltage, imbalance, harmonics, curtailment fairness

- Fits GET procurement frameworks utilities are now building, with measurable uplift and replicable deployments

5. The Path Forward: Scaling Proven Technology to Meet Market Demand

If 2025 was the year the grid became the bottleneck, 2026 is when proven solutions either scale, or miss the window.

The market signals are unmistakable:

- Utilities are reprioritising capex toward faster, more flexible solutions

- GET procurement frameworks are moving from pilot to procurement

- Connection queue pressure is forcing DNSPs to seek alternatives to traditional reinforcement

- Regulatory frameworks (Ofgem, AEMC, FERC) are explicitly supporting technologies that unlock capacity faster

The winning technologies will share three characteristics:

- Fast deployment: Months, not years

- Repeatable at scale: Hundreds or thousands of installations, not bespoke pilots

- Measurable ROI: Better cost per MW of capacity unlocked than traditional reinforcement

LV is where this battle is won. Transmission upgrades take 7-10 years. HV/MV reinforcement takes3-5 years. But LV constraints are happening now, and the window tocapture this market is narrow.

Third Equation: From Proven to Scaled

The Race for 2030 validation wasn't just a technical milestone, it was proof that NEx delivers quantifiable results in real-world conditions: zero voltage violations, 95% curtailment reduction, significant transformer loading relief.

The technology works. The market need is a cute. What comes next is execution at scale.

Third Equation is now seeking investment to:

1. Scale manufacturing anddeployment capacity

Meet utility demand for fleet-scale installations (hundreds of units annually vs. today's pilot-scale production)

2. Expand market presence

Build utility partnerships in UK, Australia, and target North American markets where LV constraints are accelerating

3. Capture first-mover advantage

The LV GET market is nascent, early entrants with proven technology and utility relationships will define the category

4. Support ongoing R&D

Continue advancing NEx capabilities (predictive controls, grid-edge intelligence, integration with flexibility markets)

The Investment Opportunity

Market timing: DNSPs are actively seeking LV solutions right now, connection queue pressure and 2030 decarbonisation targets create immediate procurement urgency.

Proven differentiation: Independent validation shows NEx outperforms incumbent solutions(STATCOMs, OLTCs) on the metrics utilities care about: voltage compliance, curtailment reduction, transformer stress relief.

Scalable business model: NEx addresses a fleet-scale problem (thousands of constrained transformers per utility) with a repeatable installation process, enabling predictable revenue growth as utility contracts scale.

Regulatory tailwinds: Grid-enhancing technologies are explicitly supported in major markets' regulatory frameworks, with capex allowances and accelerated approval processes.

Next Steps

Third Equation has moved beyond proof-of-concept. The technology is validated. The market demand is proven. The regulatory environment is favourable.

What's needed now is capital to scale deployment and capture the market window.

If you're an investor looking for infrastructure opportunities at the intersection of proven technology, urgent market need, and regulatory support, let's talk.